Does Koinly Report to the IRS? Honest Answer for Crypto Investors (2026)

This article contains affiliate links. If you sign up for Koinly through a link on this page, I may earn a commission at no extra cost to you. I only recommend tools I have genuinely evaluated.

This article is for informational purposes only and does not constitute professional tax or financial advice. Tax laws vary by country and change frequently. Consult a qualified tax professional for advice specific to your situation.

If you are about to connect your exchanges to Koinly and you are wondering whether it reports your data to the IRS — the answer is no. Koinly does not transmit your transaction data or tax calculations to the IRS or any other tax authority. It is a calculation tool that generates reports for you to submit yourself.

That said, the question matters — because the crypto tax reporting landscape in 2026 is genuinely complex, and understanding who does report to the IRS, what they report, and what your own obligations are is essential for anyone using crypto tax software. The confusion around Koinly’s role is understandable: connecting exchange API keys feels significant, and the regulatory environment is tightening fast.

After 30 years in finance, I understand the anxiety around tax compliance in a rapidly shifting regulatory environment. This guide gives you the direct answer on Koinly’s reporting role, explains the full three-party framework that governs US crypto reporting, and covers what your actual filing obligations are — regardless of what Koinly or your exchanges do.

You can import and review your transaction data on Koinly’s free plan before paying anything. Start with Koinly’s free plan here.

Quick Answer: Does Koinly Report to the IRS?

No — Koinly does not report to the IRS. It is a calculation and reporting tool that organises your transaction history, calculates your gains and losses, and generates downloadable tax reports. You decide what to submit and when. The reporting obligation in the US sits with two parties: your exchanges and brokers, who issue 1099 forms to both you and the IRS, and you, who must file Form 8949 and Schedule D with your annual tax return. Koinly’s role is to help you calculate the correct figures for that filing — it is not a reporting entity under any current US tax regulation.

Who Reports What to the IRS: The Three-Party Framework

Three parties are involved in US crypto tax reporting, each with distinct obligations. Understanding this framework makes Koinly’s role immediately clear.

| Party | Reports to IRS? | How | Your Action Required |

|---|---|---|---|

| You (the investor) | Yes — mandatory | Form 8949 + Schedule D on annual return | File every taxable event accurately |

| Your exchange (Coinbase, Kraken, etc.) | Yes — mandatory | 1099-MISC, 1099-DA (phased in from 2025) | Reconcile your filing with 1099 figures |

| Koinly | No | Not a broker — no reporting obligation | Use its reports to file accurately yourself |

The IRS treats cryptocurrency as property, meaning capital gains rules apply to every disposal — selling crypto for fiat, trading crypto-to-crypto, spending crypto on goods or services, and receiving crypto income from staking, mining, or airdrops. The digital asset question on Form 1040 requires you to answer yes if you had any crypto transactions during the year, regardless of whether you made gains or losses.

US-based centralised exchanges report to the IRS independently of anything Koinly does. When an exchange issues a 1099, one copy goes to you and one goes directly to the IRS. Koinly is not in that chain. For the complete picture of everything Koinly does and does not do, our Koinly review covers the platform in full detail.

What Happens When You Connect API Keys to Koinly?

Connecting API keys does not create any IRS reporting pathway — Koinly uses read-only access, which means the connection is a one-way data pull into its calculation engine and nothing else.

Read-only API access means the key you provide can retrieve your transaction history but cannot place orders, withdraw funds, transfer assets, or transmit data to external parties including tax authorities. There is no outbound reporting function in Koinly’s API architecture.

When creating API keys for Koinly, always verify that withdrawal and trading permissions are explicitly disabled. Most exchanges provide read-only API options specifically for tax reporting integrations. If you accidentally grant more permissions than read-only, the risk is to your exchange account security — not to any IRS reporting pathway. Koinly’s platform has no tax authority reporting function regardless of the API permission level. For a complete security analysis, our Koinly security guide covers API security in full detail.

How Form 1099-DA Changes the Picture for Koinly Users

Form 1099-DA does not make Koinly a reporting entity — but it does make accurate Koinly calculations more important than ever.

Form 1099-DA is a new IRS reporting form being phased in from 2025 that requires US crypto brokers — defined as centralised exchanges and certain other intermediaries that facilitate crypto transactions — to report customer transaction data directly to the IRS. Koinly is a software platform, not a broker. It does not facilitate crypto transactions. It processes transaction data that users import from their actual brokers and exchanges. The 1099-DA obligation falls on exchanges, not on calculation software.

The practical implication for Koinly users: your exchange will be issuing 1099-DA forms to you and the IRS simultaneously, meaning the IRS will have exchange-level data about your transactions. The gains figures on your Koinly report need to align with the exchange-reported figures on your 1099-DA forms when you file. Discrepancies between what your exchange reports and what you file are what trigger IRS notices — not the use of Koinly itself. According to IRS digital assets guidance, all crypto disposals must be reported regardless of whether a 1099 is issued.

Does Koinly Report to Tax Authorities Outside the US?

The same principle applies globally — Koinly does not transmit data to any tax authority in any country. It generates downloadable reports that you submit yourself or provide to your accountant.

For UK investors, Koinly does not report to HMRC. HMRC has its own crypto reporting framework — cryptoassets are subject to Capital Gains Tax when disposed of, and Income Tax when received as income. Koinly generates HMRC-compatible Capital Gains Summary reports for UK users. According to HMRC’s cryptoassets guidance for individuals, UK investors must report crypto gains through Self Assessment — Koinly produces the documentation needed for that process, but the filing responsibility remains with the investor.

The international regulatory trend is toward expanded exchange-level reporting rather than software-level reporting. CARF — the Crypto Asset Reporting Framework developed by the OECD — is being adopted across multiple jurisdictions and requires exchanges to report user transaction data to tax authorities. CARF obligations fall on exchanges, not on tax calculation software like Koinly.

What Koinly Actually Does With Your Data

Koinly imports your transaction history, calculates your taxable events and gains, stores the data within your account, and makes it available to you as downloadable reports. That is the complete list — there is no outbound data sharing with tax authorities or third parties.

Koinly’s privacy policy prohibits sharing user financial data with third parties for reporting purposes. Your data is used to generate your tax calculations and nothing else. The IRS does not have access to Koinly user accounts. The IRS may obtain information about your crypto activity through exchanges via 1099 forms and legal processes directed at those exchanges — but Koinly is not part of that information chain.

Your Actual IRS Filing Obligations as a Crypto Investor

The fact that Koinly does not report to the IRS does not eliminate your legal requirement to file — and in 2026, the IRS has more visibility into crypto activity than ever before.

Every US investor who had any crypto transaction in a tax year is required to answer the digital asset question on Form 1040 honestly. Every disposal — sale, trade, spend — must be reported on Form 8949 with the correct cost basis and proceeds. Every income event — staking rewards, mining income, airdrops above de minimis thresholds — must be reported as ordinary income. Koinly generates the forms and calculations that make your filing accurate and efficient, but the filing itself is your responsibility.

IRS enforcement of crypto reporting has expanded significantly with blockchain analytics partnerships, mandatory 1099-DA reporting from exchanges, and cross-referencing of exchange-reported data against filed returns. Not using structured tax software increases compliance risk by raising the probability of errors in your self-filed return — errors that the IRS can now cross-reference against exchange-issued 1099s. For a full breakdown of Koinly’s calculation accuracy, our is Koinly accurate guide covers the methodology in depth.

What To Do Next

If you are using Koinly or considering it, here is what to do this week to get your tax position in order:

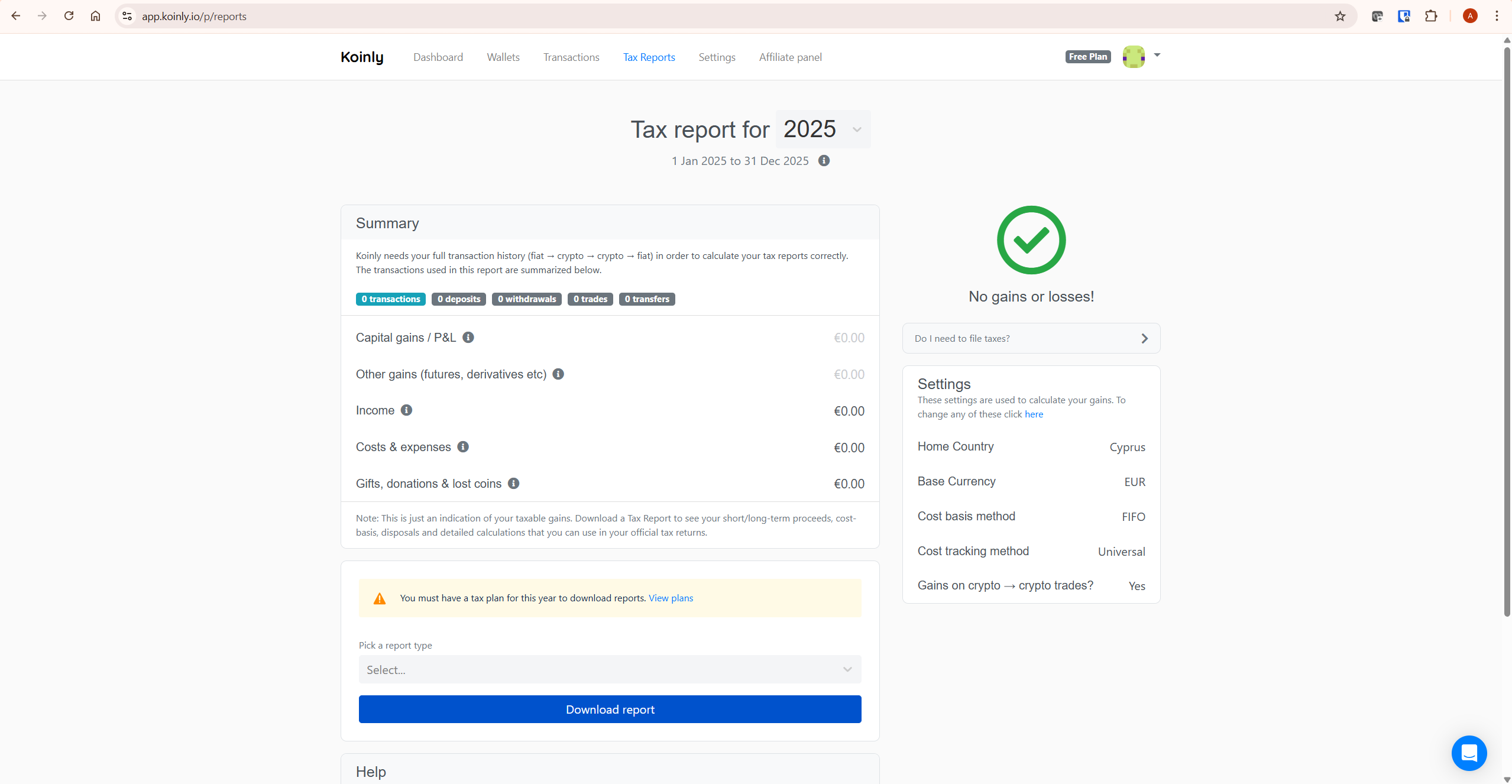

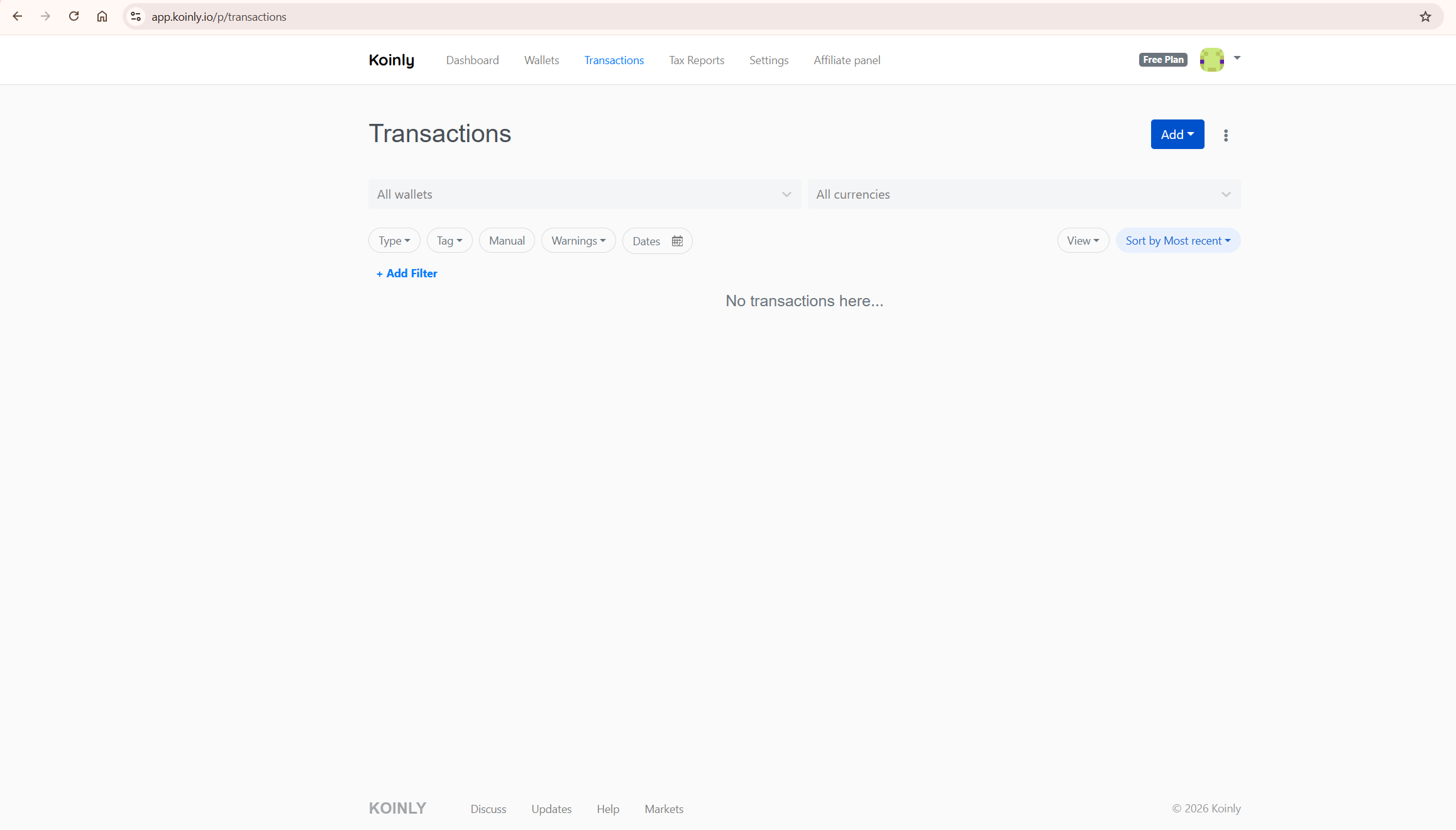

Log into Koinly and connect every exchange and wallet you used during the tax year — not just the main ones. Go to the Transactions tab and filter by Warnings. Resolve every flagged transaction before generating any report. Missing wallet connections and unresolved warnings are the two most common causes of inflated gain calculations. Once all warnings are cleared, generate your tax report and check that the capital gains figure aligns with what your exchanges have reported on any 1099 forms you have received.

If you have not started yet, Koinly’s free plan lets you import everything and review your full tax position before paying — which means you can see exactly what your filing will look like before committing to a paid report.

Frequently Asked Questions

Does Koinly report to the IRS automatically when I generate a tax report?

No — generating a report within Koinly produces a downloadable file that exists only within your account. Nothing is transmitted to the IRS at any stage of the Koinly workflow. You download the report, review it, and submit it yourself as part of your tax return filing — either directly or through your accountant.

Can the IRS access my Koinly account?

No — the IRS does not have access to Koinly user accounts. Your Koinly data is private software usage. The IRS may obtain information about your crypto activity through exchanges via 1099 forms and legal processes directed at those exchanges — but Koinly is not part of that information chain.

Does Koinly report to the IRS if my exchange issued me a 1099?

No — but it helps you reconcile the 1099 yourself. When your exchange issues a 1099 to both you and the IRS, your filed return needs to align with the exchange’s reported figures. Koinly imports your complete transaction history including the exchange data, calculates your accurate gains, and produces the Form 8949 that reconciles all your activity. Discrepancies between exchange-reported figures and filed returns are what create IRS scrutiny — Koinly helps prevent those discrepancies.

Does Koinly report DeFi and DEX transactions to the IRS?

No — and neither does anyone else currently, since decentralised exchanges are not yet subject to the same 1099 reporting requirements as centralised exchanges. However, DeFi transactions are still taxable events that you are legally required to report. Koinly imports DeFi activity from your wallet addresses and helps you calculate the correct tax treatment for swaps, liquidity pool interactions, and staking rewards. For the complete DeFi tax methodology, our Koinly DeFi and NFTs guide covers every scenario.

What happens if I do not report crypto gains that my exchange already reported to the IRS?

The IRS receives 1099 data from your exchange and cross-references it against your filed return. If your exchange reported transactions that do not appear on your return, that discrepancy can trigger an IRS notice or audit. The IRS has significantly expanded its crypto enforcement capacity since 2023, including blockchain analytics partnerships that allow it to trace wallet activity beyond what exchanges report. Filing accurately using Koinly-generated forms is your best protection against this outcome — our how to use Koinly guide walks through the complete filing workflow step by step.